United

States Securities and Exchange Commission

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

|

(x)

|

ANNUAL

REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

|

|

FOR

THE FISCAL YEAR ENDED DECEMBER 31, 2017

|

|

( )

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

|

|

|

|

FOR THE TRANSITION PERIOD

FROM

TO

|

|

|

Commission File

Number 0-1665

|

KINGSTONE

COMPANIES, INC.

(Exact name of

registrant as specified in its charter)

|

Delaware

|

36-2476480

|

|

(State or other

jurisdiction of incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

|

15 Joys Lane, Kingston, New York

|

12401

|

|

(Address of

principal executive offices)

|

(Zip

Code)

|

|

(845) 802-7900

|

|

(Registrant’s

telephone number, including area code)

|

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

Common

Stock

|

NASDAQ

|

Securities

registered pursuant to Section 12(g) of the Act:

None

Indicate by check

mark if the registrant is a well-known seasoned issuer, as defined

in Rule 405 of the Securities Act. Yes ☐ No

☒

Indicate by check

mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No

☒

Indicate by check

mark whether the registrant (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports), and (2) has

been subject to such filing requirements for the past 90 days. Yes

☒ No ☐

Indicate by check

mark whether the registrant has submitted electronically and posted

on its corporate Web site, if any, every Interactive Data File

required to be submitted and posted pursuant to Rule 405 of

Regulation S-T during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such

files). Yes ☒ No ☐

Indicate by check

mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained,

to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of

this Form 10-K or any amendment to this Form

10-K.

Indicate by check

mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated

filer,” “accelerated filer”” and

“smaller reporting company” in Rule 12b-2 of the

Exchange Act. (Check one):

|

Large accelerated

filer __

|

Accelerated filer

X

|

|

|

|

|

Non-accelerated __

(Do not check if a smaller reporting company)

|

Smaller reporting

company __

|

|

|

|

|

Emerging growth

company__

|

|

Indicate by check

mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30,

2017, the aggregate market value of the registrant’s common

stock held by non-affiliates of the registrant was $149,176,821

based on the closing sale price as reported on the NASDAQ Capital

Market. As of March 12, 2018, there were 10,684,329 shares of

common stock outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

None

INDEX

|

|

Page No.

|

||

|

2

|

|||

|

PART

I

|

|

|

|

|

3

|

|||

|

21

|

|||

|

21

|

|||

|

21

|

|||

|

21

|

|||

|

21

|

|||

|

PART

II

|

|

|

|

|

22

|

|||

|

23

|

|||

|

24

|

|||

|

63

|

|||

|

63

|

|||

|

63

|

|||

|

63

|

|||

|

66

|

|||

|

PART

III

|

|

|

|

|

66

|

|||

|

71

|

|||

|

74

|

|||

|

76

|

|||

|

77

|

|||

|

PART

IV

|

|

|

|

|

78

|

|||

|

80

|

|||

|

|

81

|

||

PART I

Forward-Looking

Statements

This

Annual Report contains forward-looking statements as that term is

defined in the federal securities laws. The events described in

forward-looking statements contained in this Annual Report may not

occur. Generally these statements relate to business plans or

strategies, projected or anticipated results or other consequences

of our plans or strategies, projected or anticipated results from

acquisitions to be made by us, or projections involving anticipated

revenues, earnings, costs or other aspects of our operating

results. The words “may,” “will,”

“expect,” “believe,”

“anticipate,” “project,”

“plan,” “intend,” “estimate,”

and “continue,” and their opposites and similar

expressions are intended to identify forward-looking statements. We

caution you that these statements are not guarantees of future

performance or events and are subject to a number of uncertainties,

risks and other influences, many of which are beyond our control,

which may influence the accuracy of the statements and the

projections upon which the statements are based. Factors which may

affect our results include, but are not limited to, the risks and

uncertainties discussed in Item 7 of this Annual Report under

“Factors That May Affect Future Results and Financial

Condition”.

Any one or more of

these uncertainties, risks and other influences could materially

affect our results of operations and whether forward-looking

statements made by us ultimately prove to be accurate. Our actual

results, performance and achievements could differ materially from

those expressed or implied in these forward-looking statements. We

undertake no obligation to publicly update or revise any

forward-looking statements, whether from new information, future

events or otherwise.

ITEM

1.

BUSINESS.

(a)

Business Development

General

As used in this

Annual Report on Form 10-K (the “Annual Report”),

references to the “Company”, “we”,

“us”, or “our” refer to Kingstone

Companies, Inc. (“Kingstone”) and its

subsidiaries.

We offer property

and casualty insurance products to individuals and small businesses

through our wholly owned subsidiary, Kingstone Insurance Company

(“KICO”). KICO is a licensed property and casualty

insurance company in New York, New Jersey, Connecticut,

Massachusetts, Pennsylvania, Rhode Island and Texas. KICO is

currently offering its property and casualty insurance products in

New York, New Jersey, Rhode Island and Pennsylvania. Although in

2017 KICO wrote 98.5% of its direct written premiums in New York,

we believe that New Jersey, Rhode Island and other states will

represent an increasing portion of the total over the next several

years.

Recent

Developments

Developments During 2017

● Public

Offering of Common Stock

In January and

February 2017, we sold a total of 2,692,500 newly issued shares of

common stock in an underwritten public offering at a public

offering price of $12.00 per share. We received net proceeds from

the public offering of approximately $30,137,000 after deducting

underwriting discounts and commissions, and other offering

expenses. Concurrently, selling shareholders sold a total of

700,000 shares of our common stock. On March 1, 2017, we used

$23,000,000 of the net proceeds from the offering to contribute

capital to KICO in support of our ratings upgrade plan and

anticipated growth, including geographic and product

expansion.

● A.M.

Best Rating

In April 2017, A.M.

Best upgraded our financial strength rating from B++ (Good) to A-

(Excellent). This upgrade means that KICO has achieved its

long-standing goal of becoming an A-rated carrier. The upgrade has

resulted in increased growth from existing agents and additional

opportunities with new agents and in new markets.

● Expanded Licensing; New Jersey,

Rhode Island and Massachusetts Expansion

In 2017, KICO

expanded its ability to write property and casualty insurance by

obtaining a license to write insurance policies in Massachusetts.

Also in 2017, KICO’s homeowners insurance products were

launched in New Jersey and Rhode Island. We began writing New

Jersey homeowners business in May and Rhode Island homeowners

business in December. We anticipate to start writing business in

Massachusetts in 2018.

● Increased Rate of Dividends

Declared

In May 2017, we

increased the quarterly dividends on our common stock from $.0625

per share to $.08 per share.

A dividend of

$.0625 per share was declared on February 7, 2017 and was paid on

March 15, 2017. Dividends of $.08 per share were declared on May

10, 2017, August 9, 2017 and November 8, 2017 and were paid on June

15, 2017, September 15, 2017, and December 15, 2017,

respectively.

● Reduced Reliance on Quota Share

Reinsurance

Effective July 1,

2017, KICO reduced the ceding percentage for its personal lines

quota share reinsurance treaty from 40% to 20%. The reduction of

the quota share ceding percentage allows KICO to retain a higher

portion of its premiums and resultant expected

profits.

● Increased Catastrophe Reinsurance

Coverage

Effective July 1,

2017, KICO increased the top limit of its catastrophe reinsurance

coverage to $320,000,000, which equates to more than a 1-in-250

year storm event according to the primary industry catastrophe

model that we follow.

● Member of the Federal Home Loan

Bank of New York (“FHLBNY”),

In July 2017, KICO

became a member of the Federal Home Loan Bank of New York

(“FHLBNY”), which provides additional access to

liquidity. Members have access to a variety of flexible, low cost

funding through FHLBNY’s credit products, enabling members to

customize advances. Advances are to be fully collateralized;

eligible collateral to pledge includes residential and commercial

mortgage backed securities, along with U.S. Treasury and agency

securities.

● Public

Debt offering

On December 19,

2017, we issued $30,000,000 of our 5.50% Senior Unsecured Notes due

December 30, 2022, in an underwritten public offering. The net

proceeds to us were approximately $29,122,000. On December 20,

2017, we used $25,000,000 of the net proceeds from the debt

offering to contribute capital to KICO, to support additional

growth. The remainder of the net proceeds will be used for general

corporate purposes. Interest will be payable semi-annually in

arrears on June 30 and December 30 of each year, beginning on June

30 2018 at the rate of 5.50% per year from December 19,

2017.

Developments During 2016

● Expanded

Licensing to Additional State; New Jersey Rate

Approval

In 2016, KICO

expanded its ability to write property and casualty insurance by

obtaining a license to write insurance policies in Rhode Island.

Also in 2016, KICO’s homeowners insurance rate, rule, and

policy form filing was approved by the New Jersey Department of

Banking and Insurance.

● A.M.

Best Rating

In 2016, A.M. Best

revised the outlook to positive from stable for the issuer credit

rating (“ICR”) of KICO. A.M. Best also affirmed

KICO’s financial strength rating of B++ (Good) and ICR of

“bbb”, and affirmed our ICR of

“bb”.

● Increased Catastrophe Reinsurance

Coverage

Effective July 1,

2016, KICO increased the top limit of its catastrophe reinsurance

coverage to $252,000,000, which at that time equated to more than a

1-in-250 year storm event according to the primary industry

catastrophe model that we follow.

● Continued

Quarterly Dividends

Dividends of $.0625

per share were declared on each of February 8, 2016, May 12, 2016,

August 11, 2016 and November 10, 2016 and were paid on March 15,

2016, June 15, 2016, September 15, 2016 and December 15, 2016,

respectively.

● Private

Placement of Common Stock

In April 2016,

we sold

595,238 newly issued shares of common stock to RenaissanceRe

Ventures Ltd., a subsidiary of RenaissanceRe Holdings Ltd.

(“RenaissanceRe”), for a purchase price of $8.40 per

share. We received $4,808,000 in net proceeds from the sale.

RenaissanceRe is a global provider of catastrophe and specialty

reinsurance and insurance.

(b)

Business

Property

and Casualty Insurance

Overview

Generally, property

and casualty insurance companies write insurance policies in

exchange for premiums paid by their customers (the

“insureds”). An insurance policy is a contract between

the insurance company and its insureds where the insurance company

agrees to pay for losses suffered by the insured that are covered

under the contract. Such contracts are subject to legal

interpretation by courts, sometimes involving legislative rulings

and/or arbitration. Property insurance generally covers the

financial consequences of accidental losses to the insured’s

property, such as a home and the personal property in it, or a

business’ building, inventory and equipment. Casualty

insurance (often referred to as liability insurance) generally

covers the financial consequences related to the legal liability of

an individual or an organization resulting from negligent acts and

omissions causing bodily injury and/or property damage to a third

party. Claims for property coverage generally are reported and

settled in a relatively short period of time, whereas those for

casualty coverage can take many years to settle.

We generate

revenues from earned premiums, ceding commissions from quota share

reinsurance, net investment income generated from our investment

portfolio, and net realized gains and losses on investment

securities. We also receive installment fee income and fees charged

to reinstate a policy after it has been cancelled for non-payment.

Earned premiums represent premiums received from insureds, which

are recognized as revenue over the period of time that insurance

coverage is provided (i.e., ratably over the life of the policy).

All of our policies are 12 month policies; therefore a significant

period of time can elapse between the receipt of insurance premiums

and the payment of insurance claims. During this time, KICO invests

the premiums, earns investment income and generates net realized

and unrealized investment gains and losses on

investments.

Insurance companies

incur a significant amount of their total expenses from

policyholder losses, which are commonly referred to as claims. In

settling policyholder losses, various loss adjustment expenses

(“LAE”) are incurred such as insurance adjusters’

fees and legal expenses. In addition, insurance companies incur

policy acquisition expenses, such as commissions paid to producers

and premium taxes, and other expenses related to the underwriting

process, including their employees’ compensation and

benefits.

The key measure of

relative underwriting performance for an insurance company is the

combined ratio. An insurance company’s combined ratio is

calculated by taking the ratio of incurred loss and LAE to earned

premiums (the “loss and LAE ratio”) and adding it to

the ratio of policy acquisition and other underwriting expenses to

earned premiums (the “expense ratio”). A combined ratio

under 100% indicates that an insurance company is generating an

underwriting profit prior to the impact of investment income. After

considering investment income and investment gains or losses,

insurance companies operating at a combined ratio of greater than

100% can also be profitable.

General; Strategy

We are a

property and casualty insurance holding company whose principal

operating subsidiary is Kingstone Insurance Company

(“KICO”), domiciled in the State of New York. We are a

multi-line regional property and casualty insurance company writing

business exclusively through independent retail and wholesale

agents and brokers (“producers”). We are licensed to

write insurance policies in New York, New Jersey, Connecticut,

Massachusetts, Pennsylvania, Rhode Island and Texas.

We seek to deliver

an attractive return on capital and to provide consistent earnings

growth through underwriting profits and income from our investment

portfolio. Our goal is to allocate capital efficiently to those

lines of business that generate sustainable underwriting profits

and to avoid lines of business for which an underwriting profit is

not likely. Our strategy is to be the preferred multi-line property

and casualty insurance company for selected producers in the

geographic markets in which we operate. We believe producers place

profitable business with us because we provide excellent,

consistent service to policyholders and claimants and provide a

consistent market with stable and competitive rate and commission

structures. We offer a wide array of personal and commercial lines

products, which further differentiate us from other insurance

companies that also distribute through our selected

producers.

Our principal

objectives are to increase the volume of profitable business that

we write while managing risk through prudent use of reinsurance in

order to preserve and grow our capital base. We seek to generate

underwriting income by writing profitable insurance policies and by

effectively managing our other underwriting and operating expenses.

We are pursuing profitable growth by selectively expanding the

geographic regions in which we operate, increasing the volume of

business that we write with existing producers, developing new

selected producer relationships, and introducing niche insurance

products that are relevant to our producers and

policyholders.

For the year ended

December 31, 2017, our gross written premiums totaled $121.6

million, an increase of 17.8% from the $103.2 million in gross

written premium for the year ended December 31, 2016.

Product Lines

Our product lines

include the following:

Personal lines - Our largest line of

business is personal lines, consisting of homeowners and dwelling

fire multi-peril, cooperative/condominiums, renters, and personal

umbrella policies. Personal lines policies accounted for 78.9% of

our gross written premiums for the year ended December 31,

2017.

Commercial liability - We offer

businessowners policies which consist primarily of small business

retail, service and office risks without a residential exposure. We

also write artisan’s liability policies for small independent

contractors with seven or fewer employees. In addition, we

write special multi-peril policies for larger and more specialized

risks businessowners risks, including those with limited

residential exposures. Further, we write commercial umbrella

policies above our supporting commercial lines policies. Commercial

lines policies accounted for 12.0% of our gross written premiums

for the year ended December 31, 2017.

Livery physical damage - We write

for-hire vehicle physical damage only policies for livery and car

service vehicles and taxicabs, primarily based in New York City.

These policies insure only the physical damage portion of insurance

for such vehicles, with no liability coverage included. These

policies accounted for 8.8% of our gross written premiums for the

year ended December 31, 2017.

Other - We write canine legal liability

policies and also have a small participation in mandatory state

joint underwriting associations. These policies accounted for 0.3%

of our gross written premiums for the year ended December 31,

2017.

Our Competitive Strengths

History of Growing Our Profitable Operations

Our insurance

company subsidiary, KICO, has been in operation in the State of New

York for over 130 years. We have consistently increased the amount

of profitable business that we write by introducing new insurance

products, increasing the volume of business that we write with our

selected producers and developing new producer relationships. KICO

has earned an underwriting profit in each of the past ten years,

including in 2012 and 2013 when our financial results were

adversely impacted by Superstorm Sandy. The extensive heritage of

our insurance company subsidiary and our commitment to the markets

in which we operate is a competitive advantage with producers and

policyholders.

Strong Producer Relationships

Within our selected

producers’ offices, we compete with other property and

casualty insurance carriers available to those producers. We

carefully select the producers that distribute our insurance

policies and continuously monitor and evaluate their performance.

We believe our insurance producers value their relationships with

us because we provide excellent, consistent personal service

coupled with competitive rates and commission levels. We have

consistently been rated by insurance producers as above average in

the important areas of underwriting, claims handling and service.

In the biennial performance surveys conducted by the Professional

Insurance Agents of New York and New Jersey of its membership since

2010, KICO was rated as one of the top performing insurance

companies in New York, twice ranking as the top rated carrier among

all those surveyed. Our relationship with selected producers was

further strengthened by the A.M. Best upgrade to a financial

strength rating of A- (Excellent) in April 2017. This has allowed

us to provide many producers with an A- rated carrier option that

was not previously available to them in the markets where we

operate.

We offer our

selected producers the ability to write a wide array of personal

lines and commercial lines policies, including some which are

unique to us. Many of our producers write multiple lines of

business with us which provides an advantage over those competitors

who are focused on a single product. We provide a multi-policy

discount on homeowners policies in order to attract and retain more

of this multi-line business. We have had a consistent presence in

the New York market and we believe that producers value the

longevity of our relationship with them. We believe that the

excellent service we provide to our selected producers, our broad

product offerings, and our consistent prices and financial

stability provide a strong foundation for continued profitable

growth.

Sophisticated Underwriting and Risk Management

Practices

We believe that we

have a significant underwriting advantage due to our local market

presence and expertise. Our underwriting process evaluates and

screens out certain risks based on property reports, individual

insurance scoring, information collected from physical property

inspections, and driving records. We maintain certain policy

exclusions that reduce our exposure to risks that can create severe

losses. We target a more preferred risk profile in order to reduce

adverse selection from risks seeking the lowest premiums and

minimal coverage levels.

Our underwriting

procedures, premium rates and policy terms support the underwriting

profitability of our personal lines policies. We apply premium

surcharges for certain coastal properties and maintain deductibles

for hurricane-prone exposures in order to provide an appropriate

premium rate for the risk of loss. We manage coastal risk exposure

through the use of individual catastrophe risk scoring and through

prudent use of reinsurance.

Our underwriting

expertise and risk management practices enable us to profitably

write personal and commercial lines business in our markets without

the need for frequent rate adjustments, in contrast to many of our

competitors. We believe that the consistency in rates and the

reliable availability of our insurance products are important

factors in maintaining our selected producer

relationships.

Effective Utilization of Reinsurance

Our reinsurance

treaties allow us to limit our exposure to the financial impact of

catastrophe losses and to reduce our net liability on individual

risks. Our reinsurance program is structured to enable us to grow

our premium volume while maintaining regulatory capital and other

financial ratios within thresholds used for regulatory oversight

purposes.

Our reinsurance

program also provides income as a result of ceding commissions

earned pursuant to the quota share reinsurance contracts. The

income we earn from ceding commissions typically exceeds our fixed

operating costs, which consist of other underwriting expenses.

Quota share reinsurance treaties transfer a portion of the profit

(or loss) associated with the subject insurance policies to the

reinsurers. We believe that a prudent reduction in our reliance on

quota share reinsurance could increase our overall net underwriting

profits.

Experienced Management Team

Our management team

has significant expertise in underwriting, agency management and

claims management. Barry Goldstein, our Chairman and Chief

Executive Officer, has extensive experience in the insurance

industry and managing public companies, serving in his current

capacity since 2001. Benjamin Walden, Executive Vice President and

Chief Actuary of KICO, has 28 years of experience with both large

and small insurance carriers and has also worked for actuarial

consulting firms. Throughout his career, he has specialized in many

of the markets that are a primary focus for KICO. Our underwriting

and claims managers have extensive experience in the insurance

industry averaging over of 28 years of experience in the markets we

serve.

Scalable, Low-Cost Operations

We focus on

keeping expenses low, but invest in tools and processes that

improve the efficiency and effectiveness of underwriting risks and

processing claims. We evaluate the costs and benefits of each new

tool or process in order to achieve optimal results. While the

majority of our policies are written for risks in downstate New

York, our Kingston, New York location provides a lower cost

operating environment. We also take a proactive approach to

settling outstanding claims rather than engaging in protracted

litigation, which results in more favorable claim outcomes and

reduced reserve uncertainty.

We have made

investments to develop online application and quoting systems for

many of our personal lines and commercial products. Since 2015, we

have leveraged a paperless workflow management and document storage

tool in order to improve efficiency and reduce costs. In late 2017,

we introduced an online payment portal that provides the ability

for insureds to make payments and to view policy information for

all of our products in one location. We now have a dedicated

customer service unit located in our Kingston office that has

significantly improved the speed at which we respond to our

customers. We have enhanced our website to improve our handling of

underwriting, claims, and billing related questions. Our ability to

control the growth of our operating and other expenses while

expanding our operations and growing revenue at a higher rate is a

key component of our business model and is important to our future

financial success.

Underwriting and Claims Management Philosophy

Our underwriting

philosophy is to target niche risk segments for which we have

detailed expertise and can take advantage of market conditions. We

monitor results on a regular basis and all of our selected

producers are reviewed by management on at least a quarterly

basis.

We

believe that our rates are competitive with other carriers’

rates in our markets. We believe that rate consistency and

the reliable availability of our insurance products is important to

our producers. We do not seek to grow by competing based

solely upon price. We seek to develop long-term relationships

with our selected producers who understand and appreciate the

consistent path we have chosen. We carefully underwrite our

business utilizing the Comprehensive Loss Underwriting Exchange

industry claims database, insurance scoring reports, physical

inspection of risks and other individual risk underwriting tools.

In the event that a material misrepresentation is discovered in the

underwriting application, the policy is voided. If a material

misrepresentation is discovered after a claim is presented, we deny

the claim. We write homeowners and dwelling fire business in

coastal markets and are cognizant of our exposure to hurricanes. We

have mitigated this risk through appropriate catastrophe

reinsurance and application of mandatory hurricane deductibles. Our

claims and underwriting expertise in these markets enables us to

profitably write personal lines business in all the territories in

which we write.

Distribution

We generate

business through our relationships with over 400 independent

producers. We carefully select our producers by evaluating numerous

factors such as their need for our products, premium production

potential, loss history with other insurance companies that they

represent, product and market knowledge, and the size of the

agency. We only distribute through independent agents and have

never sought to distribute our products direct to the consumer. We

will not appoint any agency owned or controlled by another carrier

that distributes its products direct to the consumer. We monitor

and evaluate the performance of our producers through periodic

reviews of volume and profitability. Our senior executives are

actively involved in managing our producer

relationships.

Each

producer is assigned to a personal and commercial lines underwriter

and the producer can call that underwriter directly on any matter.

We believe that the close relationship with their underwriters is a

principal reason producers place their business with us. Our

producers have access to a KICO website portal that provides them

the ability to quote risks for various products and to review

policy forms and underwriting guidelines for all lines of business.

We send out frequent “Producer Grams” in order to

inform our producers of updates at KICO. In addition, we have an

active Producer Council and have at least one annual meeting with

all of our producers.

Competition; Market

The

insurance industry is highly competitive. We constantly assess and

project the market conditions and prices for our products, but we

cannot fully know our profitability until all claims have been

reported and settled.

Our

policyholders are located primarily in the downstate regions of New

York State, but we are actively growing into nearby markets, and

introduced homeowners products in New Jersey and Rhode Island

during 2017. In addition, we are licensed to write insurance

policies in Connecticut, Massachusetts, Pennsylvania, and Texas. We

anticipate launching a homeowners product in Massachusetts in 2018.

These new homeowners markets align well with the niche markets that

have generated profitable results in New York, and we believe that

our market expertise can be effectively utilized in these new

markets.

In 2016, KICO was

the 18th largest writer of homeowners and dwelling fire insurance

in the State of New York, according to data compiled by SNL

Financial LC. Based on the same data, in 2016, we had a 1.0% market

share for this combined group of personal lines property business.

We compete with large national carriers as well as regional and

local carriers in the property and casualty marketplace in New York

and other states. We believe that many national and regional

carriers have chosen to limit their rate of premium growth or to

decrease their presence in northeastern states due to the

relatively high coastal population and associated catastrophe risk

that exists in the region.

Given present

market conditions, we believe that we have the opportunity to

significantly expand the size of our personal and commercial lines

business in New York and other northeastern states in which we are

licensed.

Loss and Loss Adjustment Expense Reserves

We are required to

establish reserves for incurred losses that are unpaid, including

reserves for claims and loss adjustment expenses

(“LAE”), which represent the expenses of settling and

adjusting those claims. These reserves are balance sheet

liabilities representing estimates of future amounts required to

pay losses and loss expenses for claims that have occurred at or

before the balance sheet date, whether already known to us or not

yet reported. We establish these reserves after considering all

information known to us as of the date they are

recorded.

Loss reserves fall

into two categories: case reserves for reported losses and LAE

associated with specific reported claims, and reserves for losses

and LAE that are incurred but not reported (“IBNR”). We

establish these two categories of loss reserves as

follows:

Reserves for reported losses - When a

claim is received, we establish a case reserve for the estimated

amount of its ultimate settlement and its estimated loss expenses.

We establish case reserves based upon the known facts about each

claim at the time the claim is reported and we may subsequently

increase or reduce the case reserves as additional facts and

information about each claim develops.

IBNR reserves - We also estimate and

establish reserves for loss and LAE amounts incurred but not yet

reported (“IBNR”). IBNR reserves are calculated in bulk

as an estimate of ultimate losses and LAE less reported losses and

LAE. There are two types of IBNR; the first is a provision for

claims that have occurred but are not yet reported or known. We

refer to this as ‘Pure’ IBNR, and due to the fact that

we write primarily quickly reported property lines of business,

this type of IBNR does not make up a large portion of KICO’s

total IBNR. The second type of IBNR is a provision for expected

future development on known claims, from the evaluation date until

the time claims are settled and closed. We refer to this as

‘Case Development’ IBNR and it makes up the majority of

the IBNR that KICO records. Ultimate losses driving the

determination of appropriate IBNR levels are projected by using

generally accepted actuarial techniques.

The

liability for loss and LAE represents our best estimate of the

ultimate cost of all reported and unreported losses that are unpaid

as of the balance sheet evaluation date. The liability for loss and

LAE is estimated on an undiscounted basis, using individual

case-basis valuations, statistical analyses and various actuarial

procedures. The projection of future claim payment and reporting is

based on an analysis of our historical experience, supplemented by

analyses of industry loss data. We believe that the reserves for

loss and LAE are adequate to cover the ultimate cost of losses and

claims to date. However, because of the uncertainty from various

sources, including changes in claims settlement patterns and

handling procedures, litigation trends, judicial decisions, and

economic conditions, actual loss experience may not conform to the

assumptions used in determining the estimated amounts for such

liabilities at the balance sheet date. As adjustments to these

estimates become necessary, such adjustments are reflected in the

period in which the estimates are changed. Because of the nature of

the business historically written, we believe that we have limited

exposure to asbestos and environmental claim

liabilities.

We engage an

independent external actuarial specialist (the ‘Appointed

Actuary’) to opine on our recorded statutory reserves. The

Appointed Actuary estimates a range of ultimate losses, along with

a range and recommended central estimate of IBNR reserve amounts.

Our carried IBNR reserves are based on an internal actuarial

analysis and reflect management’s best estimate of unpaid

loss and LAE liabilities, and fall within the range of those

determined as reasonable by the Appointed Actuary.

Reconciliation of Loss and Loss Adjustment Expenses

The

table below shows the reconciliation of loss and LAE on a gross and

net basis, reflecting changes in losses incurred and paid

losses:

|

|

Years ended

|

|

|

|

December 31,

|

|

|

|

2017

|

2016

|

|

Balance

at beginning of period

|

$41,736,719

|

$39,876,500

|

|

Less

reinsurance recoverables

|

(15,776,880)

|

(16,706,364)

|

|

Net

balance, beginning of period

|

25,959,839

|

23,170,136

|

|

|

|

|

|

Incurred

related to:

|

|

|

|

Current

year

|

34,246,081

|

27,853,010

|

|

Prior

years

|

(60,544)

|

(63,349)

|

|

Total

incurred

|

34,185,537

|

27,789,661

|

|

|

|

|

|

Paid

related to:

|

|

|

|

Current

year

|

18,194,860

|

16,496,648

|

|

Prior

years

|

9,899,802

|

8,503,310

|

|

Total

paid

|

28,094,662

|

24,999,958

|

|

|

|

|

|

Net

balance at end of period

|

32,050,714

|

25,959,839

|

|

Add

reinsurance recoverables

|

16,748,908

|

15,776,880

|

|

Balance

at end of period

|

$48,799,622

|

$41,736,719

|

Our

claims reserving practices are designed to set reserves that, in

the aggregate, are adequate to pay all claims at their ultimate

settlement value.

Loss and Loss Adjustment Expenses Development

The

table below shows the net loss development of reserves held as of

each calendar year-end from 2007 through 2017.

The

first section of the table reflects the changes in our loss and LAE

reserves after each subsequent calendar year of development. The

table displays the re-estimated values of incurred losses and LAE

at each succeeding calendar year-end, including payments made

during the years indicated. The second section of the table shows

by year the cumulative amounts of loss and LAE payments, net of

amounts recoverable from reinsurers, as of the end of each

succeeding year. For example, with respect to the net loss and LAE

reserves of $6,001,000 as of December 31, 2009, by December 31,

2011 (two years later), $3,992,000 had actually been paid in

settlement of the claims that relate to liabilities as of December

31, 2009.

The

“cumulative redundancy (deficiency)” represents, as of

December 31, 2017, the difference between the latest re-estimated

liability and the amounts as originally estimated. A redundancy

means that the original estimate was higher than the current

estimate. A deficiency means that the current estimate is higher

than the original estimate. Estimates for the liabilities in place

as of more recent evaluation dates have developed more favorably

than those from older evaluation points, especially as a percentage

of the starting estimate.

|

(in thousands of $)

|

2007

|

2008

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

2017

|

|

Reserve

for loss and loss adjustment expenses, net of reinsurance

recoverables

|

4,799

|

5,823

|

6,001

|

7,280

|

8,520

|

12,065

|

17,139

|

21,663

|

23,170

|

25,960

|

32,051

|

|

Net

reserve estimated as of One year later

|

5,430

|

6,119

|

6,235

|

7,483

|

9,261

|

13,886

|

18,903

|

21,200

|

23,107

|

25,899

|

|

|

Two

years later

|

5,867

|

6,609

|

6,393

|

8,289

|

11,022

|

16,875

|

18,332

|

21,501

|

24,413

|

|

|

|

Three

years later

|

6,433

|

6,729

|

6,486

|

9,170

|

12,968

|

16,624

|

18,687

|

22,576

|

|

|

|

|

Four

years later

|

6,569

|

6,711

|

7,182

|

10,128

|

12,552

|

16,767

|

19,386

|

|

|

|

|

|

Five

years later

|

6,683

|

7,261

|

7,766

|

9,925

|

12,440

|

16,985

|

|

|

|

|

|

|

Six

years later

|

7,245

|

7,727

|

7,602

|

9,932

|

12,367

|

|

|

|

|

|

|

|

Seven

years later

|

7,721

|

7,554

|

7,615

|

9,779

|

|

|

|

|

|

|

|

|

Eight

years later

|

7,568

|

7,511

|

7,455

|

|

|

|

|

|

|

|

|

|

Nine

years later

|

7,527

|

7,330

|

|

|

|

|

|

|

|

|

|

|

Ten

years later

|

7,347

|

|

|

|

|

|

|

|

|

|

|

|

Net

cumulative redundancy (deficiency)

|

(2,548)

|

(1,507)

|

(1,454)

|

(2,499)

|

(3,847)

|

(4,920)

|

(2,247)

|

(913)

|

(1,243)

|

61

|

|

|

(in thousands of $)

|

2007

|

2008

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

2017

|

|

Cumulative

amount of reserve paid, net of reinsurance recoverable

through

|

|

|

|

|

|

|

|

|

|

|

|

|

One

year later

|

1,855

|

2,533

|

2,307

|

3,201

|

3,237

|

4,804

|

6,156

|

8,500

|

8,503

|

9,900

|

|

|

Two

years later

|

3,339

|

3,974

|

3,992

|

4,947

|

5,661

|

8,833

|

10,629

|

12,853

|

14,456

|

|

|

|

Three

years later

|

4,339

|

5,054

|

4,659

|

6,199

|

8,221

|

11,873

|

13,571

|

16,564

|

|

|

|

|

Four

years later

|

5,146

|

5,373

|

5,238

|

7,737

|

10,100

|

13,785

|

16,166

|

|

|

|

|

|

Five

years later

|

5,424

|

5,717

|

5,997

|

8,585

|

10,903

|

15,479

|

|

|

|

|

|

|

Six

years later

|

5,738

|

6,224

|

6,562

|

8,941

|

11,417

|

|

|

|

|

|

|

|

Seven

years later

|

6,247

|

6,718

|

6,749

|

9,275

|

|

|

|

|

|

|

|

|

Eight

years later

|

6,740

|

6,853

|

7,022

|

|

|

|

|

|

|

|

|

|

Nine

years later

|

6,875

|

7,103

|

|

|

|

|

|

|

|

|

|

|

Ten

years later

|

7,123

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net

reserve -

|

|

|

|

|

|

|

|

|

|

|

|

|

December

31,

|

4,799

|

5,823

|

6,001

|

7,280

|

8,520

|

12,065

|

17,139

|

21,663

|

23,170

|

25,960

|

32,051

|

|

*

Reinsurance Recoverable

|

6,693

|

9,766

|

10,512

|

10,432

|

9,960

|

18,420

|

17,364

|

18,250

|

16,707

|

15,777

|

16,749

|

|

*

Gross reserves -

|

|

|

|

|

|

|

|

|

|

|

|

|

December

31,

|

11,492

|

15,589

|

16,513

|

17,712

|

18,480

|

30,485

|

34,503

|

39,913

|

39,877

|

41,737

|

48,800

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net

re-estimated reserve

|

7,347

|

7,330

|

7,455

|

9,779

|

12,367

|

16,985

|

19,386

|

22,576

|

24,413

|

25,899

|

|

|

Re-estimated

reinsurance recoverable

|

10,896

|

12,589

|

12,642

|

13,280

|

13,881

|

28,337

|

20,740

|

20,280

|

17,663

|

16,221

|

|

|

Gross

re-estimated reserve

|

18,243

|

19,919

|

20,097

|

23,059

|

26,248

|

45,322

|

40,126

|

42,856

|

42,076

|

42,120

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross

cumulative redundancy (deficiency)

|

(6,751)

|

(4,330)

|

(3,584)

|

(5,347)

|

(7,768)

|

(14,837)

|

(5,623)

|

(2,943)

|

(2,199)

|

(383)

|

|

See “Management’s Discussion

and Analysis of Financial Condition and Results of Operations

– Factors That May Affect

Future Results and Financial Condition” in Item 7 of this

Annual Report.

Reinsurance

We

purchase reinsurance to reduce our net liability on individual

risks, to protect against possible catastrophes, to remain within a

target ratio of net premiums written to policyholders’

surplus, and to expand our underwriting capacity. Participation in

reinsurance arrangements does not relieve us from our obligations

to policyholders. Our reinsurance program is structured to reflect

our obligations and goals.

Reinsurance

via quota share allows for a carrier to write business without

increasing its underwriting leverage above a ratio determined by

management. The business written under a quota share

reinsurance structure obligates a reinsurer to assume some portion

of the risks involved, and gives the reinsurer the profit (or loss)

associated with such in exchange for a ceding commission. We

have determined it to be in the best interests of our shareholders

to prudently reduce our reliance on quota share reinsurance.

This will result in higher earned premiums and a reduction in

ceding commission revenue in future years, but will allow us to

retain more net income from our profitable business.

Our

quota share reinsurance treaties in effect for the year ended

December 31, 2017 for our personal lines business, which primarily

consists of homeowners policies, were covered under the July 1,

2016/June 30, 2017 treaty year (“2016/2017 Treaty”) and

July 1, 2017/June 30, 2018 treaty year (“2017/2019

Treaty”) (two year treaty). The expired 2016/2017 Treaty was

at a 40% quota share percentage and the current 2017/2019 Treaty is

at a 20% quota share percentage.

Excess of loss contracts provide coverage for

individual loss occurrences exceeding a certain threshold. The

quota share reinsurance treaties inure to the benefit of our excess

of loss treaties, as the maximum net retention on any single risk

occurrence is first limited through the excess of loss treaty, and

then that loss is shared again through the quota share reinsurance

treaty. Our maximum net retention under the quota share and excess

of loss treaties for any one personal lines occurrence for dates of

loss on or after July 1, 2017 is $800,000. Commercial lines

policies are not subject to a quota share reinsurance treaty. Our

maximum net retention under the excess of loss treaties for any one

commercial general liability occurrence for dates of loss on or

after July 1, 2017 is $750,000.

We

earn ceding commission revenue under the quota share reinsurance

treaties based on a provisional commission rate on all premiums

ceded to the reinsurers as adjusted by a sliding scale based on the

ultimate treaty year loss ratios on the policies reinsured under

each agreement. The sliding scale provides minimum and maximum

ceding commission rates in relation to specified ultimate loss

ratios.

Under

the 2017/2019 Treaty and 2016/2017 Treaty, KICO is receiving a

higher upfront fixed provisional rate than in prior years’

treaties. In exchange for the higher provisional rate, KICO has a

reduced opportunity to earn sliding scale contingent

commissions.

The

2017/2019 Treaty and the 2016/2017 Treaty are on a

“net” of catastrophe reinsurance basis, as opposed to

the “gross” arrangement that existed in prior treaties.

Under a “net” arrangement, all catastrophe reinsurance

coverage is purchased directly by us. Since we pay for all of the

catastrophe coverage, none of the losses covered under a

catastrophic event will be included in the quota share ceded

amounts, drastically reducing the adverse impact that a

catastrophic event can have on ceding commissions.

In

2017, we purchased catastrophe reinsurance to provide coverage of

up to $320,000,000 for losses associated with a single event. One

of the most commonly used catastrophe forecasting models prepared

for us indicates that the catastrophe reinsurance treaties provide

coverage in excess of our estimated probable maximum loss

associated with a single more than one-in-250 year storm event. The

direct retention for any single catastrophe event is $5,000,000.

Effective July 1, 2017 losses on personal lines policies are

subject to the 20% quota share treaty, which results in a net

retention by us of $4,000,000 of exposure per catastrophe

occurrence. Effective July 1, 2017, we have reinstatement premium

protection on the first $145,000,000 layer of catastrophe coverage

in excess of $5,000,000. This protects us from having to pay an

additional premium to reinstate catastrophe coverage for an event

up to this level.

Investments

Our

investment portfolio, including cash and cash equivalents, and

short term investments, as of December 31, 2017 and 2016, is

summarized in the table below by type of investment.

|

|

December

31, 2017

|

December

31, 2016

|

||

|

|

Carrying

|

%

of

|

Carrying

|

%

of

|

|

Category

|

Value

|

Portfolio

|

Value

|

Portfolio

|

|

|

|

|

|

|

|

Cash

and cash equivalents

|

$48,381,633

|

25.8%

|

$12,044,520

|

11.2%

|

|

|

|

|

|

|

|

Held

to maturity

|

|

|

|

|

|

U.S.

Treasury securities and

|

|

|

|

|

|

obligations

of U.S. government

|

|

|

|

|

|

corporations

and agencies

|

729,466

|

0.4%

|

606,427

|

0.6%

|

|

|

|

|

|

|

|

Political

subdivisions of states,

|

|

|

|

|

|

territories

and possessions

|

998,984

|

0.5%

|

1,349,916

|

1.3%

|

|

|

|

|

|

|

|

Corporate

and other bonds

|

|

|

|

|

|

Industrial

and miscellaneous

|

3,141,358

|

1.7%

|

3,138,559

|

2.9%

|

|

|

|

|

|

|

|

Available

for sale

|

|

|

|

|

|

Political

subdivisions of states,

|

|

|

|

|

|

territories

and possessions

|

11,315,443

|

6.0%

|

8,205,888

|

7.6%

|

|

|

|

|

|

|

|

Corporate

and other bonds

|

|

|

|

|

|

Industrial

and miscellaneous

|

88,141,465

|

47.0%

|

53,685,189

|

49.9%

|

|

|

|

|

|

|

|

Residential

mortgage

backed

securities

|

20,531,348

|

10.9%

|

18,537,751

|

17.2%

|

|

|

|

|

|

|

|

Preferred

stocks

|

7,000,941

|

3.7%

|

5,685,001

|

5.3%

|

|

|

|

|

|

|

|

Common

stocks

|

7,285,257

|

3.9%

|

4,302,685

|

4.0%

|

|

Total

|

$187,525,895

|

100.0%

|

$107,555,936

|

100.0%

|

The

table below summarizes the credit quality of our fixed-maturity

securities available-for-sale as of December 31, 2017 and 2016 as

rated by Standard and Poor’s (or if unavailable from Standard

and Poor’s, then Moody’s or Fitch):

|

|

December

31, 2017

|

December

31, 2016

|

||

|

|

|

Percentage

of

|

|

Percentage

of

|

|

|

Fair

Market

|

Fair

Market

|

Fair

Market

|

Fair

Market

|

|

|

Value

|

Value

|

Value

|

Value

|

|

Rating

|

|

|

|

|

|

U.S.

Treasury securities

|

$-

|

0.0%

|

$-

|

0.0%

|

|

Corporate

and municipal bonds

|

|

|

|

|

|

AAA

|

1,358,143

|

1.1%

|

1,801,106

|

2.2%

|

|

AA

|

11,319,057

|

9.4%

|

7,236,457

|

|

|

A

|

17,199,631

|

14.3%

|

13,944,784

|

17.3%

|

|

BBB

|

68,704,768

|

57.3%

|

38,908,731

|

48.4%

|

|

BB

|

875,310

|

0.7%

|

-

|

0.0%

|

|

Total corporate and municipal bonds

|

99,456,909

|

82.8%

|

61,891,078

|

76.9%

|

|

Residential

mortgage backed securities

|

|

|

|

|

|

AAA

|

2,013,010

|

1.7%

|

-

|

0.0%

|

|

AA

|

11,021,144

|

9.2%

|

14,143,828

|

17.7%

|

|

A

|

3,902,768

|

3.3%

|

173,973

|

0.2%

|

|

CCC

|

1,420,296

|

1.2%

|

513,369

|

0.6%

|

|

CC

|

120,742

|

0.1%

|

-

|

0.0%

|

|

C

|

28,963

|

0.0%

|

112,136

|

0.1%

|

|

D

|

1,659,479

|

1.4%

|

3,594,444

|

4.5%

|

|

Non

rated

|

364,945

|

0.3%

|

-

|

0.0%

|

|

Total residential mortgage backed

securities

|

20,531,347

|

17.2%

|

18,537,750

|

23.1%

|

|

Total

|

$119,988,256

|

100.0%

|

$80,428,828

|

100.0%

|

Additional

financial information regarding our investments is presented under

the subheading “Investments” in Item 7 of this Annual

Report.

Ratings

Many insurance

buyers, agents, brokers and secured lenders use the ratings

assigned by A.M. Best and other agencies to assist them in

assessing the financial strength and overall quality of the

companies with which they do business and from which they are

considering purchasing insurance or in determining the financial

strength of the company that provides insurance with respect to the

collateral they hold. A.M. Best financial strength ratings are

derived from an in-depth evaluation of an insurance company’s

balance sheet strengths, operating performances and business

profiles. A.M. Best evaluates, among other factors, the

company’s capitalization, underwriting leverage, financial

leverage, asset leverage, capital structure, quality and

appropriateness of reinsurance, adequacy of reserves, quality and

diversification of assets, liquidity, profitability, spread of

risk, revenue composition, market position, management, market risk

and event risk. A.M. Best financial strength ratings are intended

to provide an independent opinion of an insurer’s ability to

meet its obligations to policyholders and are not an evaluation

directed at investors.

In November 2016,

we commenced a plan of action to upgrade KICO’s A. M. Best

rating. In April 2017, A.M. Best upgraded the Financial Strength

Rating (FSR) of KICO to A- (Excellent) from B++ (Good). The A.M.

Best financial strength rating of A- (Excellent) has created

significant additional demand from our existing producers,

particularly for our New York homeowners business where we compete

against many carriers that are not A- rated by A.M. Best. Other

ratings assigned to KICO and Kingstone by A.M Best and Kroll Bond

Rating Agency are as follows:

|

|

|

Kingstone

|

|

|

KICO

|

Companies

|

|

A.M.

Best Long-Term issuer credit rating (ICR)

|

a-

(stable outlook)

|

bbb-

(stable outlook)

|

|

A.M.

Best Long-Term issue credit rating (IR)

|

|

|

|

$30.0

million, 5.50% senior unsecured notes due Dec. 30,

2022

|

n/a

|

bbb-

(stable outlook)

|

|

Kroll

Bond Rating Agency insurance financial strength rating

(IFSR)

|

A-

(stable outlook)

|

n/a

|

|

Kroll

Bond Rating Agency issuer rating

|

n/a

|

BBB-

(stable outlook)

|

|

$30.0

million, 5.50% senior unsecured notes due Dec. 30,

2022

|

n/a

|

BBB-

(stable outlook)

|

KICO also has a

Demotech financial stability rating of A (Exceptional) which

generally makes its policies acceptable to mortgage lenders that

require homeowners to purchase insurance from highly rated

carriers.

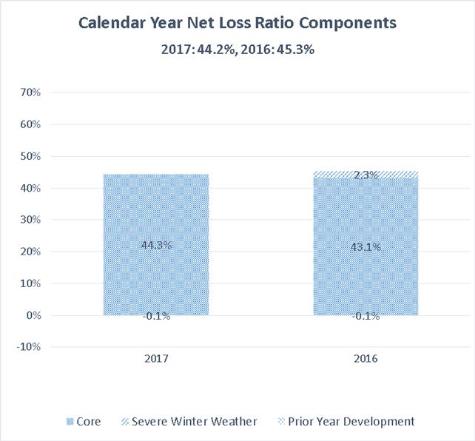

Severe Winter Weather

Our predominant

market, downstate New York, suffered severe weather during the

winter of 2016. We include severe

winter weather in our definition of catastrophe. The catastrophe

component of the 2016 severe winter was determined by the number of

claims in excess of our threshold of average claims from severe

winter weather. These claims were primarily from losses due to

frozen pipes and related water damage resulting from abnormally low

temperatures for an extended period. The effects of severe

winter weather increased our net loss ratio by 2.3 percentage

points in 2016. However, the relatively mild winter of 2017

resulted in no catastrophe impact.

The computation to

determine contingent ceding commission revenue includes direct

catastrophe losses and loss adjustment expenses incurred from

severe winter weather. Catastrophe losses for 2016 had no impact on

our contingent ceding commission revenue since the ultimate loss

ratio used to determine these commissions was not affected by the

2016 severe winter weather.

Government Regulation

Holding Company Regulation

We,

as the parent of KICO, are subject to the insurance holding company

laws of the state of New York. These laws generally require an

insurance company to register with the New York State Department of

Financial Services (the “DFS”) and to furnish annually

financial and other information about the operations of companies

within our holding company system. Generally under these laws, all

material transactions among companies in the holding company system

to which KICO is a party must be fair and reasonable and, if

material or of a specified category, require prior notice and

approval or acknowledgement (absence of disapproval) by the

DFS.

Change of Control

The

insurance holding company laws of the state of New York require

approval by the DFS for any change of control of an insurer.

“Control” is generally defined as the possession,

direct or indirect, of the power to direct or cause the direction

of the management and policies of the company, whether through the

ownership of voting securities, by contract or otherwise. Control

is generally presumed to exist through the direct or indirect

ownership of 10% or more of the voting securities of a domestic

insurance company or any entity that controls a domestic insurance

company. Any future transactions that would constitute a change of

control of KICO, including a change of control of Kingstone

Companies, Inc., would generally require the party acquiring

control to obtain the approval of the DFS (and in any other state

in which KICO may operate). Obtaining these approvals may result in

the material delay of, or deter, any such transaction. These laws

may discourage potential acquisition proposals and may delay, deter

or prevent a change of control of Kingstone Companies, Inc.,

including through transactions, and in particular unsolicited

transactions, that some or all of our stockholders might consider

to be desirable.

State Insurance Regulation

Insurance

companies are subject to regulation and supervision by the

department of insurance in the state in which they are domiciled

and, to a lesser extent, other states in which they conduct

business. The primary purpose of such regulatory powers is to

protect individual policyholders. State insurance authorities have

broad regulatory, supervisory and administrative powers, including,

among other things, the power to grant and revoke licenses to

transact business, set the standards of solvency to be met and

maintained, determine the nature of, and limitations on,

investments and dividends, approve policy forms and rates, and in

some instances to regulate unfair trade and claims

practices.

KICO

is required to file detailed financial statements and other reports

with the insurance regulatory authorities in the states in which it

is licensed to transact business. These financial statements are

subject to periodic examination by the insurance

regulators.

In

addition, many states have laws and regulations that limit an

insurer’s ability to withdraw from a particular market. For

example, states may limit an insurer’s ability to cancel or

not renew policies. Furthermore, certain states prohibit an insurer

from withdrawing from one or more lines of business written in the

state, except pursuant to a plan that is approved by the insurance

regulatory authority. The state regulator may disapprove a plan

that may lead to market disruption. Laws and regulations, including

those in New York, that limit cancellation and non-renewal and that

subject program withdrawals to prior approval requirements may

restrict the ability of KICO to exit unprofitable markets. Such

laws did not affect KICO’s ability to withdraw from the

commercial auto market in New York State in 2015.

Federal and State Legislative and Regulatory Changes

From

time to time, various regulatory and legislative changes have been

proposed in the insurance industry. Among the proposals that either

have been or are being considered are the possible introduction of

Federal regulation in addition to, or in lieu of, the current

system of state regulation of insurers, and proposals in various

state legislatures (some of which proposals have been enacted) to

conform portions of their insurance laws and regulations to various

model acts adopted by the National Association of Insurance

Commissioners (the “NAIC”).

In

2017, the DFS implemented new comprehensive cybersecurity

regulations which became effective on March 1, 2017 with

transitional implementation periods. When fully implemented, the

regulations require covered entities, including KICO, to establish

a cybersecurity policy, a chief information security officer,

oversight over third party service providers, penetration and

vulnerability assessments, secure systems to maintain an audit

trail, risk assessments to include access privileges to nonpublic

information, use of multi-factor authentication, and an incident

response plan, among other provisions. Commencing February 15,

2018, and annually thereafter, KICO must certify compliance to the

DFS with the applicable cybersecurity regulatory

provisions.

In

2010 the Dodd-Frank Wall Street Reform and Consumer Protection Act

(the “Dodd-Frank Act”) became law. It established a

Federal Insurance Office (the “FIO”) within the U.S.

Department of the Treasury. The FIO is initially charged with

monitoring all aspects of the insurance industry (other than health

insurance, certain long-term care insurance and crop insurance),

gathering data, and conducting a study on methods to modernize and

improve the insurance regulatory system in the United States. In

December 2013, the FIO issued a report (as required under the

Dodd-Frank Act) entitled “How to Modernize and Improve the

System of Insurance Regulation in the United States” (the

“Report”), which stated that, given the

“uneven” progress the states have made with several

near-term state reforms, should the states fail to accomplish the

necessary modernization reforms in the near term, “Congress

should strongly consider direct federal involvement.” The FIO

continues to support the current state-based regulatory regime, but

will consider federal regulation should the states fail to take

steps to greater uniformity (e.g., federal licensing of insurers).

In 2017, the new President indicated that the provisions of this

law should be reviewed. In its September 2017 Annual Report on the

Insurance Industry, FIO provided a survey of Insurance Industry

Financial Overview, Domestic Regulatory and Market Developments,

and U.S. Competitiveness in Global Markets.

State Regulatory Examinations

As

part of their regulatory oversight process, state regulatory

authorities conduct periodic detailed examinations of the financial

reporting of insurance companies domiciled in their states,

generally once every three to five years. Examinations are

generally carried out in cooperation with the insurance regulators

of other states under guidelines promulgated by the NAIC. The New

York DFS commenced its examination of KICO in 2016 as of December

31, 2015. The examination was completed in 2017 and had no material

adverse findings.

Risk-Based Capital Regulations

State

regulatory authorities impose risk-based capital

(“RBC”) requirements on insurance enterprises. The RBC

Model serves as a benchmark for the regulation of insurance

companies. RBC provides for targeted surplus levels based on

formulas, which specify various weighting factors that are applied

to financial balances or various levels of activity based on the

perceived degree of risk, and are set forth in the RBC

requirements. Such formulas focus on four general types of risk:

(a) the risk with respect to the company’s assets (asset

or default risk); (b) the risk of default on amounts due from

reinsurers, policyholders, or other creditors (credit risk);

(c) the risk of underestimating liabilities from business

already written or inadequately pricing business to be written in

the coming year (underwriting risk); and (d) the risk

associated with items such as excessive premium growth, contingent

liabilities, and other items not reflected on the balance sheet

(off-balance sheet risk). The amount determined under such formulas

is called the authorized control level RBC

(“ACL”).

The

RBC guidelines define specific capital levels based on a

company’s ACL that are determined by the ratio of the

company’s total adjusted capital (“TAC”) to its

ACL. TAC is equal to statutory capital, plus or minus certain other

specified adjustments. KICO’s TAC is far above the ACL and is

in compliance with New York’s RBC requirements as of December

31, 2017.

Dividend Limitations

Our ability to receive dividends from KICO is

restricted by the state laws and insurance regulations of New York.

These restrictions are related to surplus and net investment

income. Dividends are restricted to the lesser of 10% of

surplus or 100% of investment income (on a statutory accounting

basis) for the trailing 36 months, less dividends by KICO paid

during such period.

Insurance Regulatory Information System Ratios

The

Insurance Regulatory Information System (“IRIS”) was

developed by the NAIC and is intended primarily to assist state

insurance regulators in meeting their statutory mandates to oversee

the financial condition of insurance companies operating in their

respective states. IRIS identifies thirteen industry ratios and

specifies “usual values” for each ratio. Departure from

the usual values on four or more of the ratios can lead to

inquiries from individual state insurance commissioners as to

certain aspects of an insurer’s business.

As

of December 31, 2017, as a result of its growth and the $23 million

and $25 million contributions of capital we made to KICO in March